My recent post about the development of the retail archive at the University of Stirling mentioned that there are various donations that are being processed, though this may take some time. The archive is built around the 40+ year history of the Institute for Retail Studies and the research we undertook, but has also received donations from those who were external to this work in the University.

The archive is a little eclectic in the sense that it contains core material on retail change but also material based on the things that we worked on or were interested in at that time. In due course my collection of Argos catalogues will be deposited in the archive. These are an illustration of the serendipity of the collection.

In addition to filling in gaps in the Argos collection to complete the unique record from, and then after, the initial donation, media publicity around the catalogues has in itself produced interesting donations.

One of these (from Martin Lamb) was a personal shopping diary kept for a period of over twenty years, recording, by one of his relatives, each shopping trip and what products purchased, often with till receipts. Whilst uniquely personal, insights from it can be of interest (see our academic article here) and it illustrates well the changing nature of retail choice.

It was after another radio programme on Argos catalogues that the focus of this post was offered as a donation and accepted. I took a phone call from Harry and Sue Levine who were clearing their attic and who wanted to see if we had use for a collection of retail bags extending over a long period. Obviously we jumped at the offer. As with catalogues, such retail ephemera too often goes missing and is lost to history.

We are currently photographing and storing the bags. They are a distinctive collection of retail brand and design history. I hope in due course to publish all the photographs, probably initially via social media. The selection of photographs below provides a snapshot:

Such donations add to the richness of our archive and allow us to capture some of the detail of retailing that would otherwise (as is so often the case) be lost. I am always interested if people want to get in touch to offer retail artefacts. We may not be able to take everything but will love the chance to discuss possibilities.

Green Shield Stamps could be traded in for ‘free’ gifts so why did consumers abandon them?

Sean Farrington examines their rise and fall and discovers how they spawned a famous retail chain which is still trading. The stamps were the centrepiece of an early form of loyalty scheme and were collected by tens of millions of people across the UK. They were given out by shops with every purchase and could be exchanged for a wide range of household goods and luxury items from handbags to vacuum cleaners and even cars.

The BBC Business journalist, Sean Farrington, speaks to expert guests including:

Sir John Timpson – chairman of the retail services provider, Timpson, who dedicated a chapter of his book on ‘High Street Heroes’ to the Green Shield Stamp founder, Richard Tompkins.

Professor Leigh Sparks – Professor of Retail Studies at the University of Stirling.

Alongside them, analysing the stamps’ fortunes is the entrepreneur, Sam White.

In September 1983 I arrived at Stirling to seek out somewhere to live before I took up a job at the University. I had been to Scotland once before, but that was a rugby weekend, and memories even then were scanty or embargoed, to say the least. I almost got killed by a Co-op milk lorry in West Wales on the way back, but that’s another tale, though it explains my aversion to the Co-op for a decade or so.

Six months or so after arriving in Stirling we got married and ended up in St. Ninians and have never really moved away. At the time I had six months on my contract so never imagined I would still be at the University some 41 years later.

I’ve been a Professor since 1992, and led the Institute for Retail Studies, the Department of Marketing, and the Stirling Management School before, after something of a hiatus (aka a seven-year sulk), becoming Founding Head of Stirling Graduate School and since 2016 a Deputy Principal.

It’s been a blast. Having a job that allows me to use the few skills I have and to follow my research, retail and towns/place interests has been a privilege. But there comes a time to wind down and call it a day, and 41 years is a good innings. For context, the University has been open 57 years!

So, I have decided it is time to retire from the University at the end of September 2024.

No doubt I will reflect on the last 41 years at Stirling at some point, but until September I am focusing on my Deputy Principal role, which is more than enough.

In the short time I had in Singapore this January, we decided to continue to seek out the old amongst the new. It was, as I noted last year in my piece on shophouses good to see pockets of old Singapore being preserved (and valued).

Shophouses again featured on my list of things to look for, and I remain fascinated by the tiles and tiling. Whilst I was too late/disorganised to book a tour of the NUS Baba House, and so missed out on seeing inside it, the area around (Blair Plain) was a delight to wonder and to look at what survives. It was interesting to see a few sites being redeveloped, but having to conserve the key features of the existing buildings.

It was not just shophouses though. Staying in a hotel in one of the shophouse areas makes one look at surrounding buildings. The 1920s/1930s was a great design period in Singapore, and quite a few traces of the art-deco (tropical deco according to some) influence remain here.

One of the buildings I had always wanted to take a better look at was The Majestic Theatre in Chinatown. This looks like an art deco masterpiece but is no longer a theatre (seems to be a senior citizen centre and home of a gambling organisation). The art-deco motifs are obvious but have seen better days. Some of the modern additions have driven right through the tiling etc in a hugely unsympathetic way. This is a real shame.

Elsewhere in Chinatown there were some attempts to inform people about the retail history of key shops. Some of the old photos and artefacts were really interesting. The same approach was seen in Little India as well, which also has a rather colourful merchant’s house. For most though I suspect the history gets in the way – you don’t know what you’ve got till it’s gone.

A final item – the ever excellent museums in Singapore have some great artefacts and I was especially taken by the exhibition of items recovered from an ancient merchant ship. This was an amazing collection of Chinese ceramics and included a lovely bowl and a translation of its inscription. Retail branding alive and well a thousand years ago.

As I think I have mentioned, I was away in January, mainly in Cambodia, but also in Singapore. Since I have been back it has been a little hectic and so some posts reflecting on aspects of my time away have been a little delayed.

In Cambodia we were based in Phnom Penh and Siem Reap, and no that is not going to mean lots of temple photos in this blog (though I do have a lot of them). My focus here is on the markets we visited and saw and the roles they play.

In Phnom Penh the 1930s (though renovated later) Central Market was a fabulous space, reminiscent in its dome of the Pantheon in Rome. The market was a mixture of lots of stalls in a relatively open plan, though sectioned, setting with food and flowers on the outside. It seemed to attract both locals and of course tourists. The Russian Market was a denser network of stalls, as was the main market in Siem Reap.

Travelling around, and away from some of the touristed areas, one could not help to see the influence and importance of markets in Cambodian life. The suburban and village markets were the hubs of local life and daily routine. The produce looked great in most cases. They attracted huge volumes of motorbike traffic.

In Singapore markets are likewise important though modern stores have made big inroads. The government has also sought to tidy up the markets from what I recall in the late 1980s. When I visited in October, the Tekka Market in Little India was closed for refurbishment and I did fear for it.

On visiting in January it was back, and as lively and vibrant as ever, both in the market stalls and the Hawker centre/prepared food section. I was very pleased to see the spice stall I have visited for years still in operation.

And finally on the theme of market vibrancy and centrality to people, here are some photos a friend sent me from Goa. The same idea and importance.

We really have lost so much of our food culture and life in so many parts of the UK, and are the poorer for it. These Asian markets show how the local food networks provide for supply and local economic engagement. There are of course many contextual differences to the UK, but when you think what our food supply looks like, one has to question the direction we are taking. This is not the case everywhere but we could do worse than investing locally in proper market facilities and supporting those who produce for them.

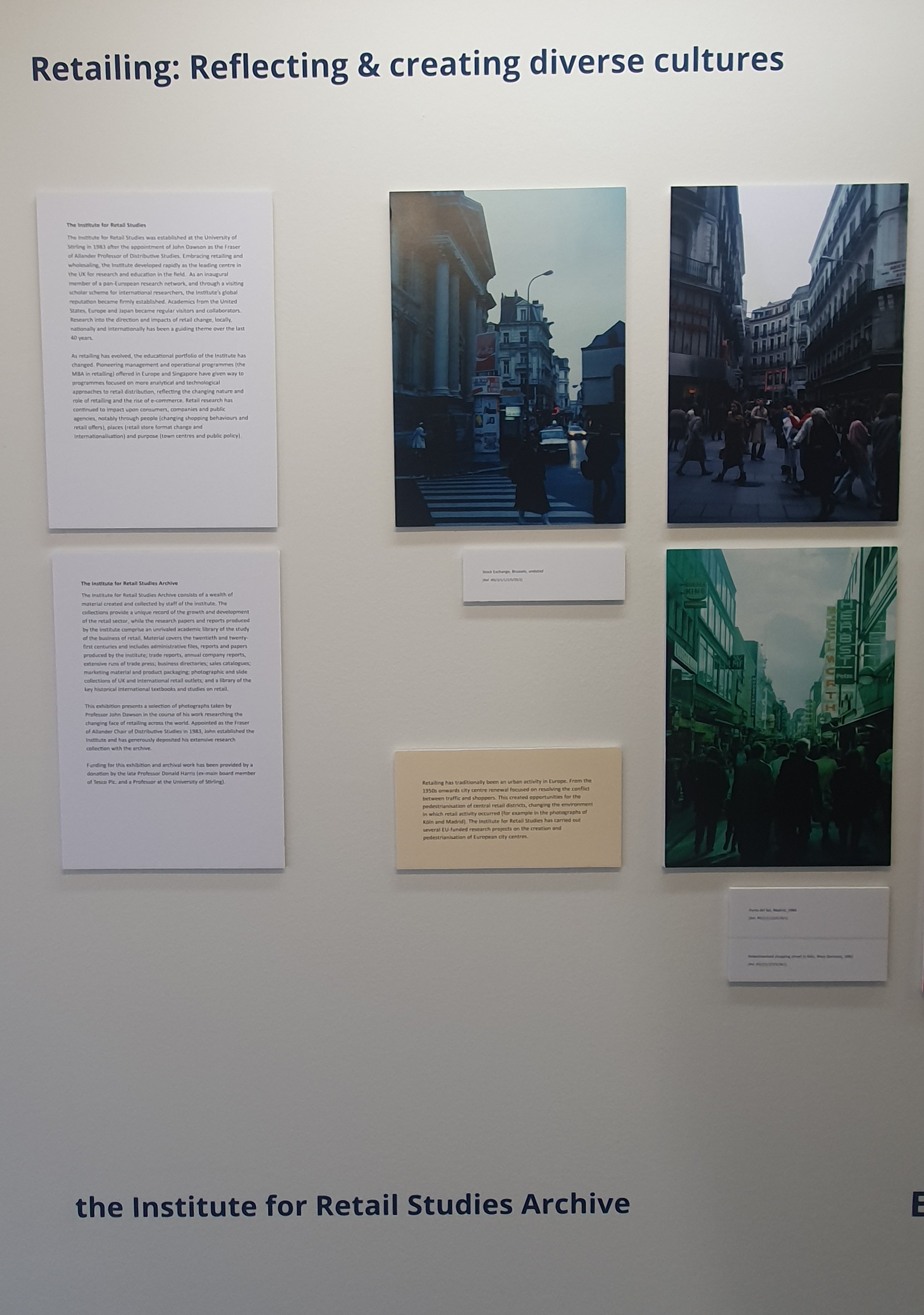

Anyone entering the library at the heart of the University of Stirling in recent weeks can not help but notice the latest use of the exhibition space. It’s been taken over by us retailers, to celebrate 40 years of retail research and education at the University.

The Institute for Retail Studies (IRS) has put on a small exhibition of archive material. The exhibition, which runs until Thursday, 28 March, shows how retailing has changed over the last four decades, with a display of photos and product packaging from the collections held within the Institute’s extensive archive.

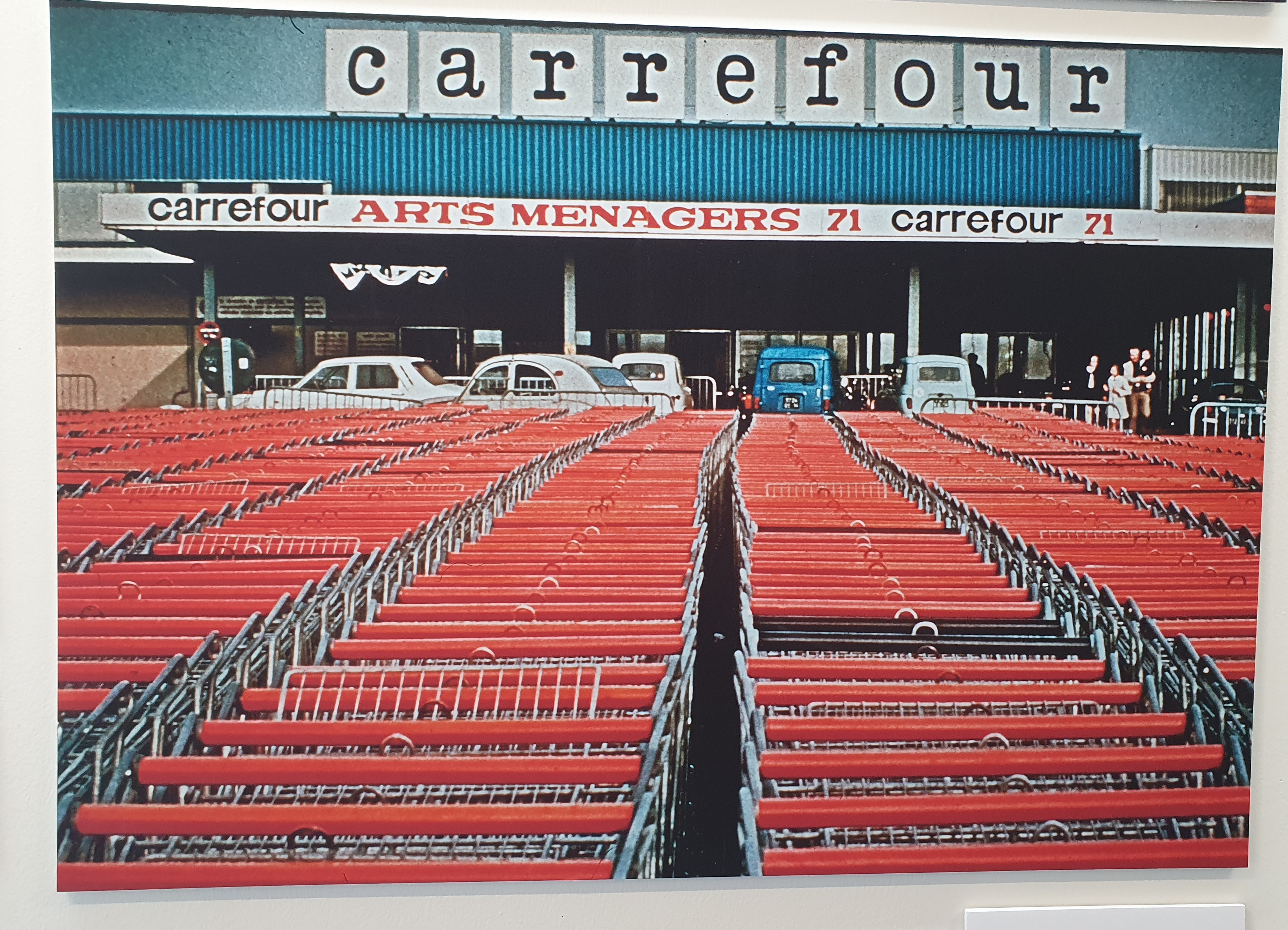

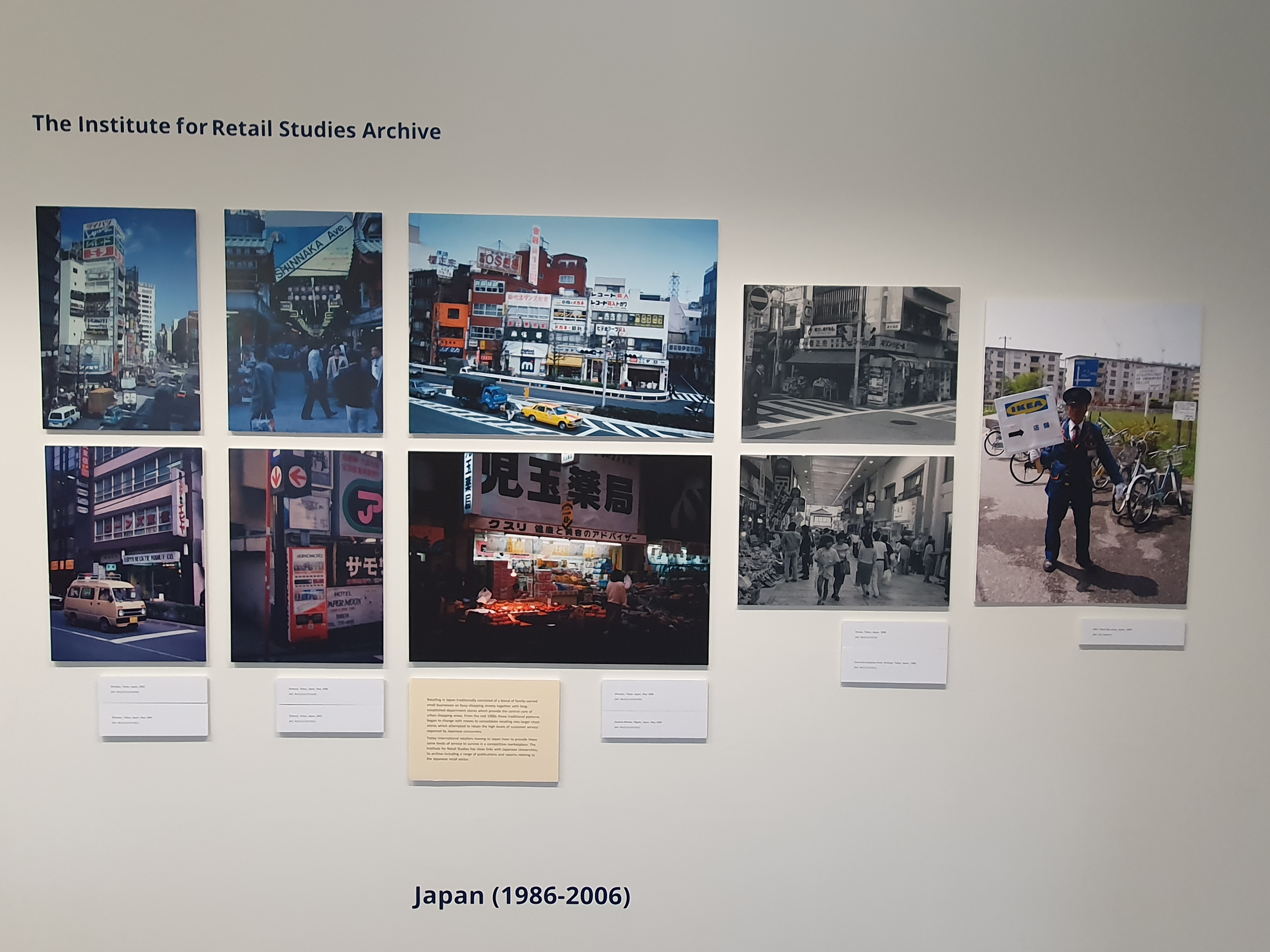

The Institute for Retail Studies was established at the University of Stirling in 1983 after the appointment of John Dawson as the Fraser of Allander Professor of Distributive Studies, who was described in the press as ‘Britain’s first Professor of Shopping’. The Institute developed rapidly as the leading centre in the UK for research and education in the field. As an inaugural member of a pan-European research network, and through a visiting scholar scheme for international researchers, the Institute’s global reputation became firmly established. Academics from the United States, Europe and Japan became regular visitors and collaborators. Research into the direction and impacts of retail change, locally, nationally and internationally has been a guiding theme over the last 40 years.

University of Stirling Archivist Karl Magee said: “We were delighted to work with the Institute to create this exhibition which showcases how their research has documented the changes in the retail environment across the world. The exhibition illustrates in particular the international research carried out by Professor Dawson, captured in the extensive photographic collection he has donated to the archive, and demonstrates how the day-to-day products we consume are carefully marketed and designed in the examples of supermarket packaging from Professor Steve Burt’s collection.”

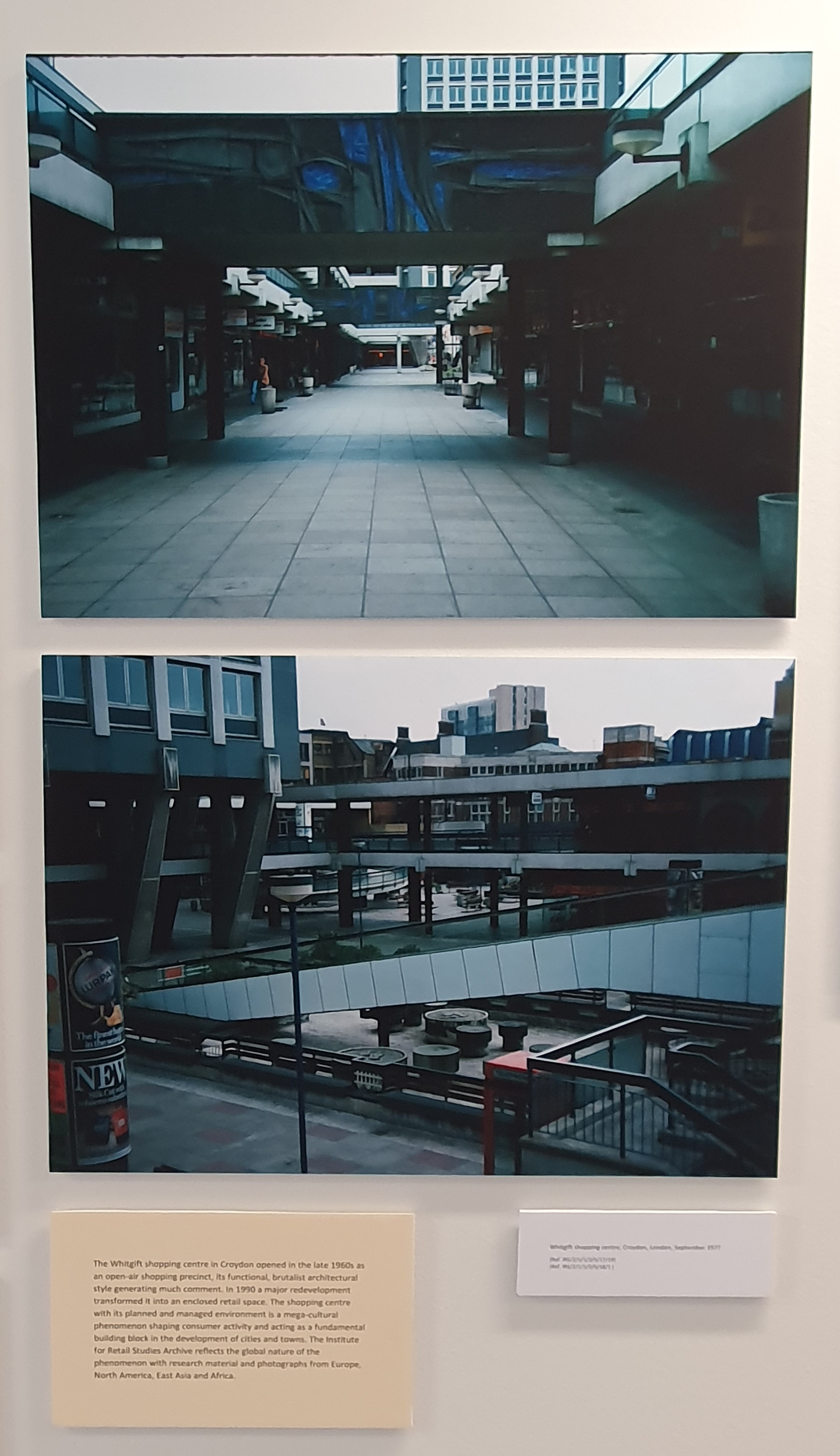

As retailing has evolved, the educational portfolio of the Institute has changed. Pioneering management and operational programmes (the MBA in retailing) offered in Europe and Singapore have given way to programmes focused on more analytical and technological approaches to retail distribution, reflecting the changing nature and role of retailing and the rise of e-commerce. Retail research has continued to impact upon consumers, companies and public agencies, notably through people (changing shopping behaviours and retail offers), places (retail store format change and internationalisation) and purpose (town centres and public policy).

The Institute for Retail Studies Archive

The Institute for Retail Studies Archive consists of a wealth of material created and collected by staff of the institute. The collections provide a unique record of the growth and development of the retail sector, whilst the research papers and reports produced by the institute comprise an unrivaled academic library of the study of the business of retail. Material covers the twentieth and twenty-first centuries and includes administrative files, reports and papers produced by the institute; trade reports, annual company reports, extensive runs of trade press; business directories; sales catalogues; marketing material and product packaging; photographic and slide collections of UK and international retail outlets; and a library of key historical international textbooks and studies on retail.

This exhibition presents a selection of photographs taken by Professor John Dawson in the course of his work researching the changing face of retailing across the world. John has generously deposited his extensive research collection with the archive. The archive is under development with donations of material also received from academic colleagues within the Institute, and external contributors such as leading retail analyst Nick Bubb.

Funding for this exhibition and archival work was provided by a donation by the late Professor Donald Harris, a former board member of Tesco and Professor at the University of Stirling.

At present only the core (Dawson and Bubb) collections have been archived. Material of a range of forms, items and artefacts have been donated from various other people and are being accessioned along with Stirling academic contributions, including in due course my Argos collection. If anyone has items they feel might be of interest please get in touch with me (leigh.sparks@stir.ac.uk).

Early January 2024 marked 15 years from the collapse of Woolworths in the UK and the closure of its 807 mainly high street stores. There are several potential parents of the phrase ‘death of the high street’, spanning many decades, but for many the failure of the iconic Woolworths is the true signifier of retail change/high street collapse (depending on your view).

On the 10th anniversary of the failure I wrote a piece on this blog about the collapse and the aftermath. I drew heavily on the work of the expert in this field Graham Soult (@soult) and his report on the fate of the stores 10 years on. In the interim 5 years Woolies has continued to fascinate and the nostalgic spectacles are often on view suggesting the need for its rebirth.

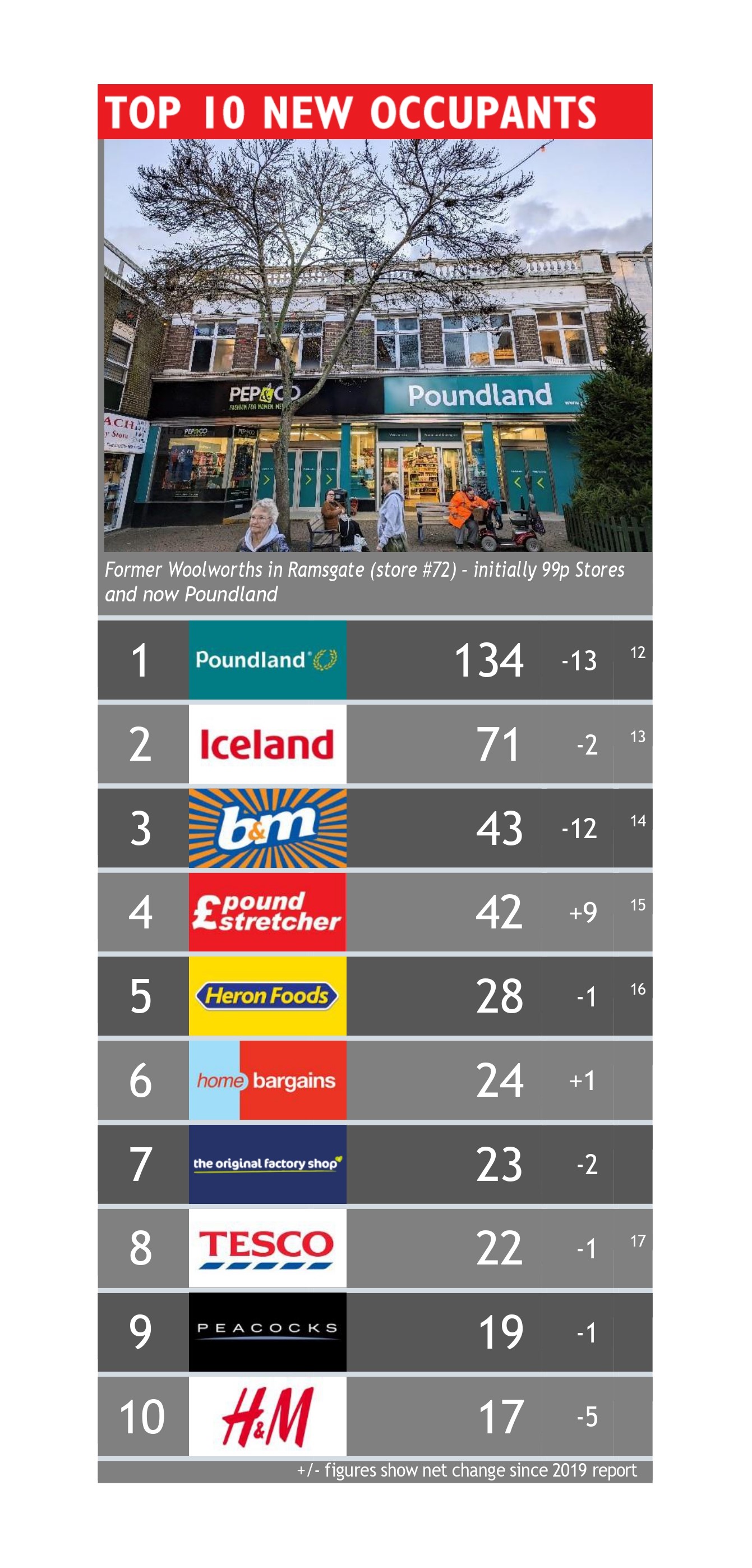

Well, it is now 2024 and we get to do it all again, as Graham Soult has updated his work and produced a report on Woolies 15 years on. As before it is meticulously researched and documented and has a wealth of detail and discussion on various issues and locations. If you have not seen it you can download a copy from the cannyinsights website.

I can’t do justice to the report’s detail in this post but amongst the headlines are:

83% of Woolies stores remain in use by other retailers;

c40% of the sites house discount variety stores i.e. stores with a Woolies type offer;

20% of sites are now convenience grocers;

Over the last 5 years there are fewer fashion occupiers, more subdivision and more independent users;

There is more non-retail use than in 2019 and a growing number of sites have a housing component;

48% of the locations have the same tenant that took over 15 years ago.

At one level none of this is surprising; many of the trends are nationally and sectorally recognisable. But perhaps the stability is remarkable, though given the site locations and store buildings of many Woolworths, perhaps not? They were/are a key part of many towns’ streetscapes.

A final thought: in my previous blog post I questioned the nostalgia for Woolworths and suggested, using their own data, that for 20+ years they had been haemorrhaging customers. Many had already walked away from Woolies, so their collapse affected fewer retail customers than assumed – and that niche was filled quickly by B&M, Poundland and so on. Nostalgia was alive and well in 2009. For Woolies workers it was a disaster, but for their customers, was it really? Or is it (was it) mostly nostalgia and hype?

Woolworths collapsed in 2009. No one under 15 has ever seen one in real life. By 2008 their active customer base (of by then 4.5 million) was less than a third of 20 years prior. In 2024 how many of the British population of today have actually shopped in a Woolworths? As people know I am all for a bit of nostalgia, but it needs to be based on some reality, and I am not sure Woolworths is a viable phoenix. There are reasons they lost two-thirds of their customer base in a 20 year period.

Graham Soult’s work on this is really interesting and useful and it is well worth a read. But perhaps more for what it says about retail and high street change than for Woolworths.

At this time of year, I often post about my recent reading, generally on the theme of retail books. This year though there is a different theme. Normal service will be renewed in due course.

I grew up in South Wales in the 1960s. The back of my car, Scottish number plate and all, has a Cofiwch Dryweryn sticker which has sparked a few conversations about why we should Remember Tryweryn. It has special relevance these days as the “UK Government” sidelines, diminishes and re-colonises the “devolved” nations. Not much has changed in my lifetime in that regard.

My detailed knowledge of the events of the 1960s onwards and the fight for rights, bilingualism, S4C etc is somewhat lacking. It was a soundtrack of my growing up, but in the background and a little muted. Yet reading some recent books has brought more of that period out for me, and sharpened things I was aware of, at the time.

Tryweryn: A New Dawn?: The Legacy of the Drowning of Capel Celyn is an even-handed and detailed account of the saga of the drowning of Lake Dryweryn by Liverpool Corporation and the role of various political and other actors of the time. It draws out the conflict, as well as the conflicted nature of looking for purely binary divides. But what was done and how it was done, remain shameful.

Brittle with Relics: A History of Wales, 1962–97 is an oral history that is much less even-handed. It documents in words, by those that were often there, the struggles for identity and the reactions to a range of events in Wales from the 1960s. From Tryweryn, the investiture, Aberfan, bilingual road signs, S4C, the miners strikes, the referendum on the (now) Senedd, the changing social and economic nature of the country, overlain by language and sense of difference, it captures my sense of otherness. And that is something I value in the Scotland I have lived in for 40 years. There is an alternative to a Westminster approach; one that is more grounded in concern for people, their lives and their culture and identity.

In October we visited the National Museum at St. Fagans. I had been there before, but not for some time. It was October, it was wet, but the buildings remain hugely interesting. The Oakdale Workmen’s Institutewas a highlight as was seeing The Vulcan Hotel re-emerging as a pub next door. The Ewenny Kiln comes from a few hundred yards from where I lived, and the Gwalia Stores (my retail link for today) is from the Ogmore Valley. But it is bittersweet; these buildings were the hearts of communities, and those communities are diminished in so many ways.

But what also captured me were the galleries and their renditions of changing Wales including again Tryweryn, Aberfan, the investiture but also more recent gender and ethnic politics and the current rise in football interest through the Wal Goch. In some ways it was Brittle with Relics in visual form and quite combative (for some) in its content and approach to national identity (rightly so). Compare and contrast to the other ‘National’ Museums around the rest of the UK and London.

The visit did make me think about the founding of St. Fagans and encouraged me to turn to the recent book on Iorwerth Peate, (Man, Myth and Museum: Iorwerth C. Peate and the Making of the Welsh Folk Museum). The story, the myth, the battles (petty squabbles) and the fight for the Folk Museum was unknown to me. St. Fagans had just always been there as I grew up (yet it was only established a few years before my birth). Many aspects of discussing what a Folk Museum should be, and whether it should cover industrial heritage and life, were especially interesting, particularly given the rural/industrial dichotomy of Wales. But an abiding thought was the way the language was written into St. Fagans’ development by Peate. Without that, so much might have been different (and reduced).

That sense of struggle permeates these three books. Often the struggle is with those ‘outside’. In some cases though, the fight is with those inside Wales or parts of its culture and identity – a claustrophobia born of power dynamics and small men in control. The power mechanisms of the national bodies (as seen in the Iorwerth Peate story), the lack of ‘groundedness’ and not seeing that change is needed, brings us to the final book – Seimon Williams’s tale for the ages of clinging on to the past (in so many bad ways) in Welsh Rugby (WELSH RUGBY: What Went Wrong?). Not much in the book is new to those who inhabit Gwladrugby, but to see it all brought together and laid out in one place hammers home the catalogue of disastrous mis-steps that have brought Welsh rugby to its knees. If (and even I now think it is a question) rugby is a key component of Welsh identity, then the face revealed is ugly and unfit for 2023/4 (and indeed well before that). How could so few get so much wrong? And keep on thinking they were right? It isn’t new and it isn’t all about personal gain, but is so often about dismissing “others” who think or look different.

Four different books, but with chords that resonate across them. What is identity and how do we forge new structures, models, organisations when it is so contested, despised (by some) and challenging to the powers that have been for so long? Whilst about Wales and its (our) idiosyncrasies, the themese could be about so many people, places and countries.

It’s that time of year again. The blog is another year older, but certainly not any wiser. At this point I normally reflect on the visitor activity on the blog during the year – and this year is going to be no different.

In terms of volume of visitors, the blog has attracted almost the same level as last year (within one percent of last year’s total), making it the fourth highest year since it started. Thanks to all those that visited.

The main measure of activity I have used previously has been the top10 or so posts in the year. As always there is an interesting mixture of new and old posts (6/4 this year). The themes of interest are broadly the same though as last year:

Grocery Market Shares: A recurring theme in the blog has been grocery market shares and their changing levels. This is always a topic of interest, and probably the most attractive to students. Twenty One Years of UK Grocery Market Shares (#1) and UK Grocery Market Shares 1997-2019 (#3) show the highest level of visitors on this topic this year and are big draws. My most recent post on the topic – Grocery Market Shares in Great Britain 1997-2023 – comes in at #9 (but it was only posted in late July and owes this position to a late run in December). I find it interesting that the UK is a bigger draw in search terms than GB, though the latter is the more accurate for that data set.

History: Two long-standing posts on aspects of retail history again feature in the top10 as they did last year. London’s Welsh Dairies turns up at #2 which is a bit of a surprise and a post on Co-operative Tokens, Sports Direct and the Bristol Pound (#8) also continues to do well. Niche subjects can attract a following, but Welsh Dairies having such an attraction is curious and delightful.

There is obviously a recency bias to looking at the past year and 6 out of the 10 are posts within 2023. But in looking at an ‘all-time’ (i.e. since 2011) top10 the same themes emerge if we strip out the visits to the home page, the page about me (why people?), downloadable articles and book detail pages, which dominate overall visits.

I started the blog to allow me to write some short commentary material and to hopefully have some data in one place that people (journalists, students etc) might find useful. Next April will mark 13 years of doing it. I’ve had fun mostly and I hope it has been, and continues to be, of interest to some others.

Retailing has been going through a challenging time in the last three or four years. The restrictions and disruption of Covid have given way to an extreme cost-of-living crisis and an almost apocalyptic sense of uncertainty on a geo-political level. The end of days in so many ways.

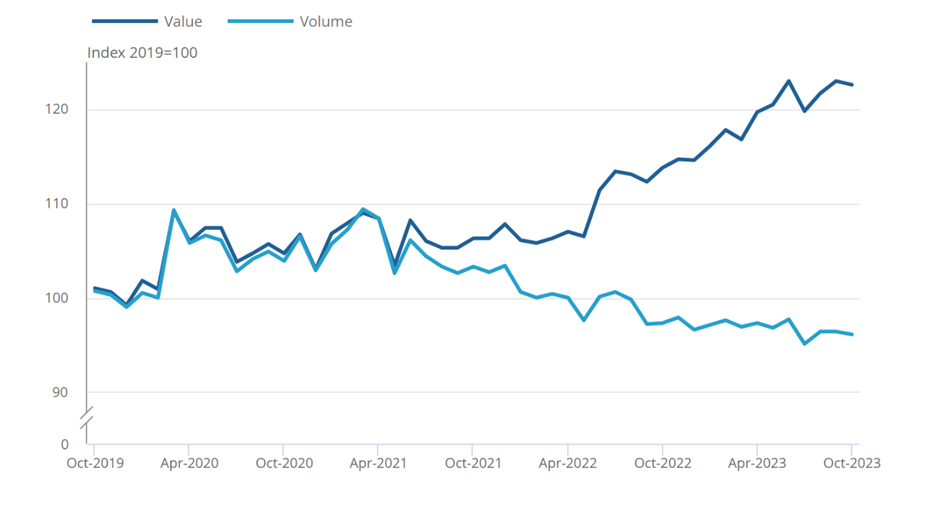

Retailers are struggling with everyday trade and making ends meet due to ever rising costs of doing business and consumers less willing to spend and looking either for a bargain or to cut their spending. This is obviously a generalisation and some consumers and some retailers are doing fine, but many are not. Reduction (and it will continue) in disposable income in the UK, the fight with inflation, Covid and a decade plus of austerity have altered capacity and actions. We see this starkly currently in the divergence of value and volume sales (in grocery in the diagram below).

Christmas though is meant to be a celebratory period, with scope to provide a relief for both consumers and retailers. The last three years have been a real balancing act due to restrictions and crises.

Well, they asked me again and the Economics Observatory published my efforts on the 14th December. The original can be found here. As before, reading the full post there is best. If you want to see them together then all my Economics Observatory and Conversation pieces on the topic can be found here.

There is undoubtedly money around and people are out celebrating Christmas and buying presents and treats. Some retailers as ever will do well. But there are more people than ever struggling and concerned in the wake of cost-of-living, inflation and interest rate rises. The disparities are now enormous and deeply worrying and cut through society, economy and geography at many levels. We need these addressed in both a more radical and sustained way. Some particular end of days can’t come quickly enough.